Discover more about S&P Global’s offerings

COVID-19's impact on the global economy and consumer behaviors has reduced long-term world oil demand by 2.5 million barrels per day, according to S&P Global Platts Analytics Future Energy Outlooks.

However, some adjustments to the demand outlook were positive as weaker oil prices make electric vehicles less competitive, reduce the drive for efficiency, and stimulate underlying oil consumption.

The weaker oil demand therefore is not meaningful enough to substantively bring forward the timing of the peak in oil demand that S&P Global Platts Analytics projects for the late 2030s. For oil demand to peak by 2025, drastic changes would need to occur to business and consumer behavior, including near full adoption of working from home, reshoring of supply chains, and widespread electrification of road transportation.

Together with added COVID-19 concerns regarding ESG risks, weaker forecasts for oil demand are forcing oil companies to reassess investments and policies.

The oil majors, which have the size and financial power to do so, might decide to develop renewables that would offer them options for adapting to changing energy scenarios, build different power assets, or gradually consolidate.

Editor's Note: This report on the Energy Transition, published by S&P Global Ratings and S&P Global Platts Analytics, is a thought leadership report that neither addresses views about ratings nor is a rating action. S&P Global Ratings and S&P Global Platts are divisions of S&P Global.

Petroleum’s pre-eminence as a land, air, and marine transport fuel is seeing oil consumption drop the most of all primary energy sources amid the global economic downturn that started this year. The unprecedented collapse in worldwide mobility as a result of lockdowns and travel restrictions in March and April 2020 slashed oil demand by over 20 million b/d, or 20% of total demand. We expect global oil demand for 2020 as a whole to decline by 8.1 million b/d, wiping out six years of growth. We expect about 75% or 6.3 million b/d of demand to come back in 2021.

The unprecedented cut to demand was met with an unprecedented cut to supply. After initial disagreement and delay, OPEC+ implemented decisive cuts, which allowed the market to start rebalancing and restored some confidence, although maintaining discipline may not be easy for the cartel. Producers inside and outside of OPEC+, facing their second crisis in five years, responded by slashing capex, costs, and shareholder returns.

While the global oil market will rebound considerably as the world economy recovers and lockdowns ease, the disruptions to both global oil demand and supply will persist far after the pandemic has ended, with considerable implications for the energy transition. For demand, individuals and businesses forced to reduce travel during lockdowns have identified potential long-lasting cost savings that will both blunt the recovery in consumption and reduce long-term demand. Many businesses have made working from home arrangements permanent to reduce real estate needs and costs, and have signaled that business travel will be reduced for the foreseeable future as well. The recession also raised inequality, with a shift of part of the middle class into poverty, which has triggered a drop in demand on its own, perhaps as high as 400,000 b/d.

Partly offsetting these negative impacts, are the following: There could be an aversion to public transportation in favor of personal vehicles if fears of virus transmission persist. Additionally, weaker oil prices make electric vehicles (EVs) less competitive than internal combustion engine vehicles and will slow their penetration relative to the pre-COVID forecast. More broadly, a weaker oil price framework will insulate oil demand from competitive threats, including a drive for efficiency improvements. And finally, there is the elasticity of demand, as a $10 a barrel lower oil price could raise oil consumption by 2.5-3.5 million b/d.

While S&P Global Platts Analytics projects that 2021 global oil demand will regain approximately 75% of the 2020 demand loss, we do not project overall consumption to return to pre-COVID-19 levels until late 2022 and believe long-term demand for oil has been permanently altered. Some sectors, most notably aviation, will take even longer to recover to pre-COVID-19 levels. The reduction in demand was driven by both our revised weaker macroeconomic outlook, and the assumption of a modest change in behaviors listed above. The weaker oil demand forecast averages out to a drop of 2.5 million b/d over 2020-2050. However, while the outlook for global oil demand has shifted lower, the trajectory of year-to-year growth and the projected peak in oil demand near 2040 remains similar to the pre-COVID-19 outlook.

On the supply side, cuts to capital expenditures and specific project delays will lead to a reduction in non-OPEC (non-shale) production well into the mid-2020s and have even longer-lasting repercussions if producers require higher price signals relative to project breakevens to commit to new supply. We expect the combination of COVID-19 and the oil price collapse to halve growth in non-OPEC supply (outside of the U.S. and Russia). For U.S. shale, the reduction in the rig count and overall activity, coupled with the relatively steep decline rates of shale wells, will result in a slow recovery of output, and S&P Global Platts Analytics projects that U.S. crude and condensate supply will not return to 2019 levels until late 2023 or early 2024. Even after this period, weaker demand and price projections have reduced the outlook for U.S. shale by an average of 900,000 b/d over 2025-2040. For OPEC+, the reduction in supply in 2020 was greater than that of non-OPEC, although S&P Global Platts Analytics projects that OPEC+ can bring supply back to the market when demand and price dictate than non-OPEC can. This flexibility will advantageous because the recovery of oil demand and non-OPEC oil supply will almost assuredly not be synchronized. However, even the forecast of OPEC+ output was reduced from the pre-COVID-19 forecast due to the severity of the projected demand decline, but by a relatively small amount compared to non-OPEC.

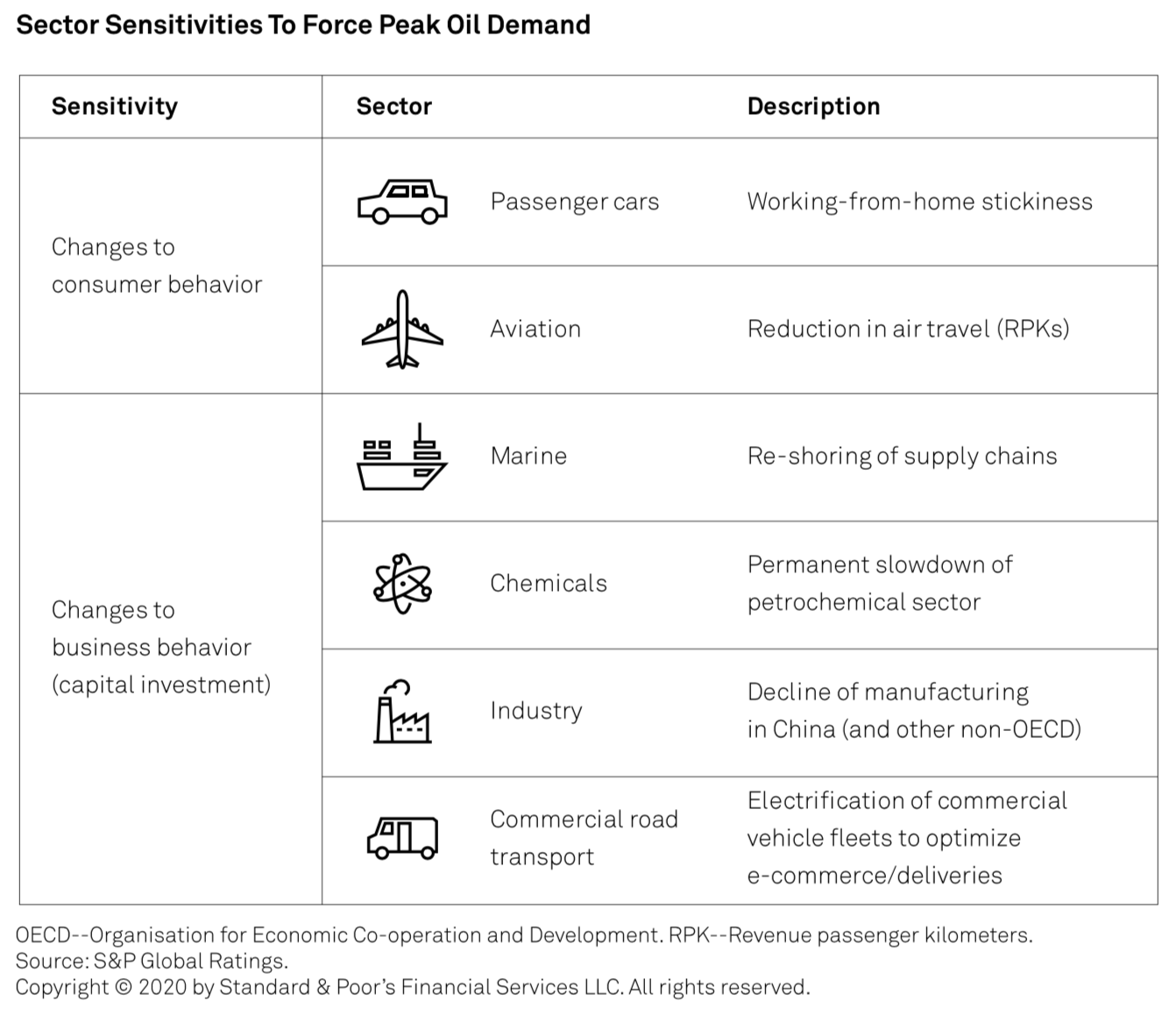

For both long-term global oil demand and supply, the impact of COVID-19 is a decided step down, but not a step change--that is, not enough to alter the trajectory of the oil market enough to meaningfully bring forward the peak in oil demand, or align oil sector CO2 emissions with a 2-degree warming target. However, the global economy and oil market are still reeling from the pandemic, and it's unclear how much behavior and policy will change in response. In an attempt to address these risks, S&P Global Platts Analytics undertook a sensitivity analysis to determine what potential changes to consumer behavior and capital investment would force oil demand to perpetually remain below the 2019 peak.

As opposed to S&P Global Platts Analytics’ Most Likely Case that concludes that up to 3 million b/d of long-term oil demand is at risk due to changes in discretionary travel, this peak demand sensitivity makes harsher assumptions on discretionary travel such as full working-from-home stickiness. Specifically this assumes that remote work becomes the status quo following the pandemic, representing up to 25% of vehicle miles traveled in the U.S. (and a similar impact outside of the U.S.). A similar severe reduction in aviation demand was adopted in this sensitivity, with a baseline rate of over 4% a year halving to just over 2% a year, implying that the world will only approach pre-pandemic levels of air travel by 2030 (whereas our baseline assumptions assumes so by 2024).

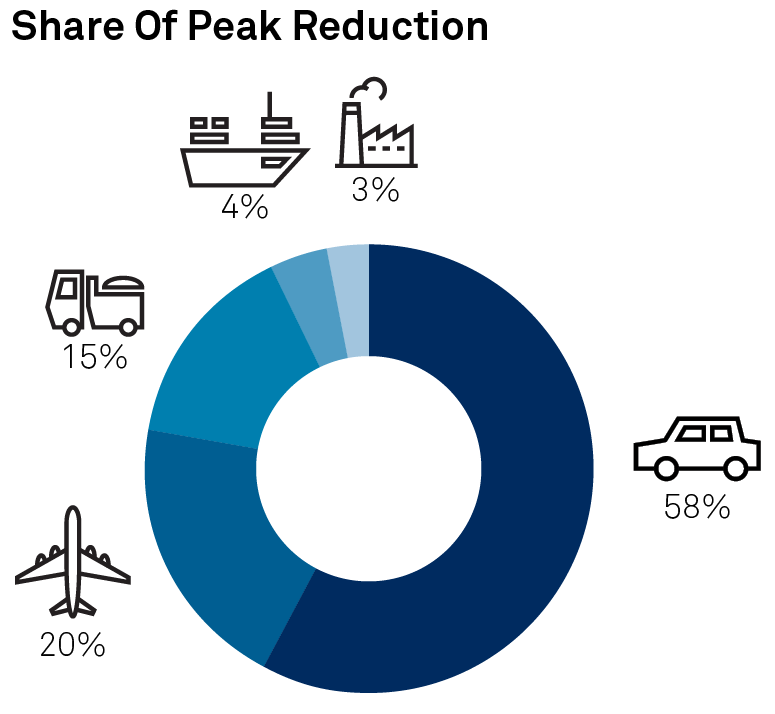

Downward pressures on oil demand as a result of changes to capital investment could persist in a post-pandemic world across several sectors, including marine bunkers, industrial demand (manufacturing), chemicals, and even commercial road transport. We project oil demand in marine bunkers to grow steadily through 2040 in our analysis of supply-demand balances due to more rapid economic growth and, in turn, international trade. In this peak demand sensitivity, S&P Global Platts Analytics projects that anti-globalization trends will accelerate, modeled as a 50% reduction in the forecasted globalization index from 2020-2025 versus our Most Likely Case. This sensitivity also assumes reshoring of supply chains away from countries where oil use is high in the industrial sector, specifically China, Saudi Arabia, and Mexico. Finally, in terms of capital investment decisions, evolving shopping patterns could have a material change on commercial road fleets. As part of a market-driven response to the complete shift away from brick-and-mortar retail to online shopping after 2020, delivery fleet operators could seek to electrify delivery trucks and vans, building upon the landmark partnership between Amazon and commercial EV manufacturer Rivian. Taken together, all of these modeled trends point to a world that could see peak oil demand by 2035 instead of 2040. When excluding petrochemical feedstocks, that is, refined products, demand could peak as early as 2025 (versus 2035 in the base case). However, we note that this scenario hinges primarily on changes to market behavior that are not necessarily market driven, but are rather discretionary or related to risk aversion.

Prior to COVID-19, the inevitability of the global energy transition represented a disruptive future for oil and gas companies. COVID-19, in many aspects, may have brought this future forward. Indeed, the pandemic created the second severe sector downturn in five years and the third in 12 years. Not surprisingly, default activity has spiked again.

While COVID-19 will not abruptly usher in a new world order, it has forced oil and gas companies to reassess future investments and price assumptions, accepting that weaker demand is likely to keep oil prices lower over the long term. The latter has caused some majors to report large write-downs to their assets, due to numerous projects being no longer commercially viable under their revised prices. Because of this, combined with mounting ESG concerns, oil majors could reduce investments in traditional oil projects in favor of clean energy investments, in 2020 and beyond. This is one of the shifts in BP’s revised strategy.

We believe cash flow from oil and gas companies may be even less certain in the coming decades than in the past 10 or 20 years. Although S&P Global Ratings factors in a price recovery to a $50-$55/bbl range in 2023 on the back of supply-demand rebalancing, COVID-19 has further underscored the increased risk of behavioral change causing a lower-for-longer oil price scenario, such as the one presented above by S&P Global Platts Analytics. Even if we still see such a stress scenario as unlikely, it is one of several factors weighing on our business risk assessments of oil and gas majors. (See also "Write-Downs, While Eye-Catching, Are Not The Largest Issue Facing Oil And Gas Supermajors," Aug. 3, 2020).

A prevailing thought among analysts is that lower oil prices caused by the pandemic could test oil companies' commitment to renewable energy investment given the strain on budgets. However, cuts to renewable energy by the largest players have been nominal, especially outside the U.S. Indeed, several firms like Total and Eni have reaffirmed their commitments to renewable investment and as a percentage of total spending, renewable spending actually increased. We recognize that renewables remain a modest percentage of overall budgets, but all major oil companies have slashed capital expenditure plans and announced severe cost-cutting measures. In some cases, majors like Shell, BP, and Equinor have slashed dividends that had long been considered sacrosanct.

Trends in investor sentiment, ESG-related pressures, and policy developments will likely only increase after the pandemic, and influence strategies and longer-term investment decisions in renewables. Over the last six years, the oil and gas industry has been one of the worst-performing sectors in the S&P 500. In response, oil companies have been forced to cut their capital spending budgets to improve cash flow and deliver higher returns to an investment community that has stopped clamoring for production growth and grown weary of volatile and weak fossil fuel prices. As for public policies, the EU's 2050 net-zero carbon emission policy partly explains why European majors are further along the renewable investment path than U.S majors. BP has explicitly signaled that as part of its new strategy, while hydrocarbon production will decline 40% to 1.5 million b/d of oil equivalent by 2030, its renewable power generation will increase 20 fold from 2.5 GW in 2019 and it will increase the number of EV charging points by nearly 10x to 70,000. The U.S. majors have made far less of an effort to move away from fossil fuel investment, in part because there has been very little incentive to do so from government. Nonetheless, this could potentially change after the November election if former Vice President Joe Biden were to win the presidency. He has pledged $2 trillion to eliminate all greenhouse gases from the electricity grid before 2035.

Investing in renewables is, however, a double-edge sword. Ironically, reduced profits from oil and gas can make capital allocation to--historically lower-yielding--renewables a less dilutive prospect for group earnings. Still, for companies used to putative double-digit returns from oil and gas upstream projects, it remains a tough choice to invest in assets that are priced in an extremely competitive manner. We see generally only high single-digit returns, and often only achievable after adding significant financial leverage and increased debt-related risks--on or off the balance sheet. We believe indications of future returns are just that, but Shell has pointed to a 12%-14% as a range for renewable projects. BP has guided group return on adjusted capital employed (ROACE) increasing to 12%-14% in 2030 from 8.9% in 2019. This implies some value could be added through integration into other group businesses, compared with stand-alone renewable projects. The increasing size of renewable projects (notably offshore wind) and policy shifts to reduce subsidies or to shorten fixed-price protection may represent an opportunity for large, well-funded new entrants. At the same time, risks in merchant power should not be underestimated, notably when lacking a diversified generation mix or downstream integration. In some respects, BP's steps into solar two decades ago were just too early. This shows the difficulty of developing and delivering the right offering in the right place at the right time. It's fair to say that we don't see an immediate "new energy" replacement for the potential large value creation of a successful oil and gas appraisal.

Oil and gas companies might turn to testing other energy markets and business models at a manageable scale, that would provide diversification from fossil fuels and options with which to adapt to changes in energy scenarios. These can include expanding gas and power trading operations and downstream integration into power retail operations. The latter is particular important to reduce the extreme volatility of power generation. Two examples in 2018 included Shell's purchase of First Utility in the U.K. and Total's acquisition of Direct Energie in France. Deploying EV recharging facilities to maintain traffic at retail sites is another adaptation. Clearly, the oil majors also have a competitive strength in offshore projects and execution of large projects, making offshore wind an attractive growth area. Finally, the development of carbon capture storage technology and related commercialization of hydrogen would support their gas business, but European policies strongly favor green hydrogen (generated through renewable electricity). Finally, the massive size and financial strength of the oil majors may position them best as future consolidators and leaders of a broader energy industry—not just as hydrocarbon players. Oil producers can make their production processes a bit greener and offset their Scope 1--and even Scope 3--emissions. But they need to become energy, not just oil and gas companies, if they want to really change their colors.

The prices and assumptions that S&P Global Ratings uses, for the purposes of its ratings analysis, may differ from those that S&P Global Platts reports. Data that S&P Global Platts uses includes independent and verifiable data collected from actual market participants. Any user of the data should not rely on any information and/or assessment therein in making any investment, trading, risk management, or other decision.

This report does not constitute a rating action.