Discover more about S&P Global’s offerings

Published: January 5, 2021

This report is reprinted from Panjiva, part of S&P Global Market Intelligence. Download this report here.

The report reviews the events that were emblematic of the changes in trade policy, logistics sector and industrial supply chain operations in 2020, based on our monthly most-read research review and the c1,200 reports published by Panjiva research in 2020. For each report we outline what it covered, why it mattered and what the data told us, with charts updated for the most recent data available.

January – Come for the commitments, stay for the enforcement

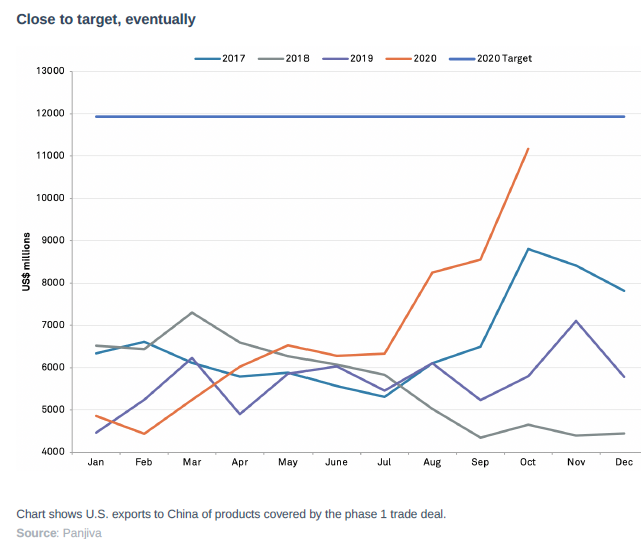

The event: The U.S. and China signed their long-awaited phase 1 trade deal including a wide range of commitments from China to increase purchases of U.S. goods and reform economic policy while the U.S. committed to modestly scaling back tariffs.

Why it mattered: The signing effectively paused hostilities and tariff escalation that had been ongoing since July 2018 and brought a degree of planning certainty for supply chains. It certainly didn’t bring peace to relations between the two with continued U.S. sanctions against Chinese suppliers ranging from electronics to cotton throughout the year.

What the data showed: China’s purchasing commitments would require an 88.4% uplift in U.S. exports of manufactured goods ranging from autos and aerospace to pharmaceuticals and machine tools throughout the year. Our ongoing research through the year showed China has been consistently behind target.

February – Coronavirus delivers a blow to the logistics sector

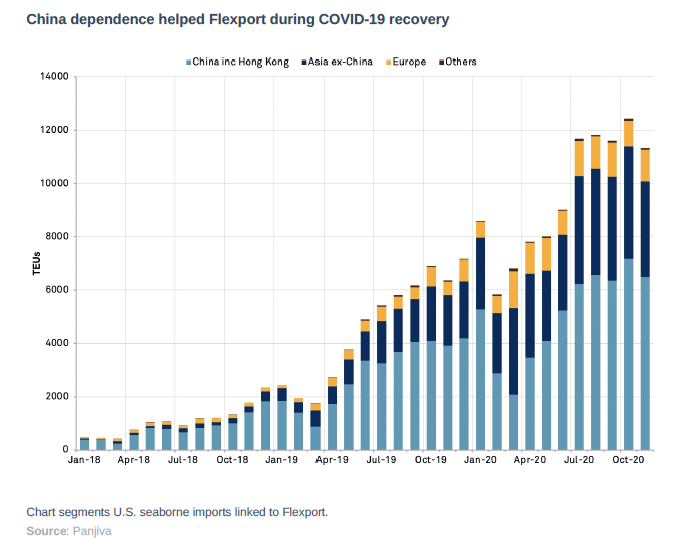

The event: Panjiva Research has published over 250 articles regarding the impact of the COVID-19 pandemic on global supply chains and logistics operations since January. In February the virus was still an epidemic centered on China but container-lines including Maersk, CMA-CGM and ONE have all discussed cutting capacity from Asia to Europe while Flexport and DP-DHL warned of a loss of “belly capacity” in airfreight.

Why it mattered: In 2016 a moderate downturn in demand for shipping resulted in widespread financial losses for the shipping industry. In 2020 the sector as a whole showed discipline throughout the pandemic in cutting capacity via blank-sailings. It did a less good job for seafarers, many of whom have struggled to return home as countries applied travel restrictions.

What the data showed: The initial impact on logistics firms was dependent in part on their exposure initially to China-outbound shipments, though global shipping volumes soon declined. We compared DP-DHL and Flexport. China represented 52.2% of Flexport’s U.S.-to- China seaborne volumes in 2019 compared to 31.4% for DP-DHL.

March – Contraction, commitments and containers – the oil price collapse

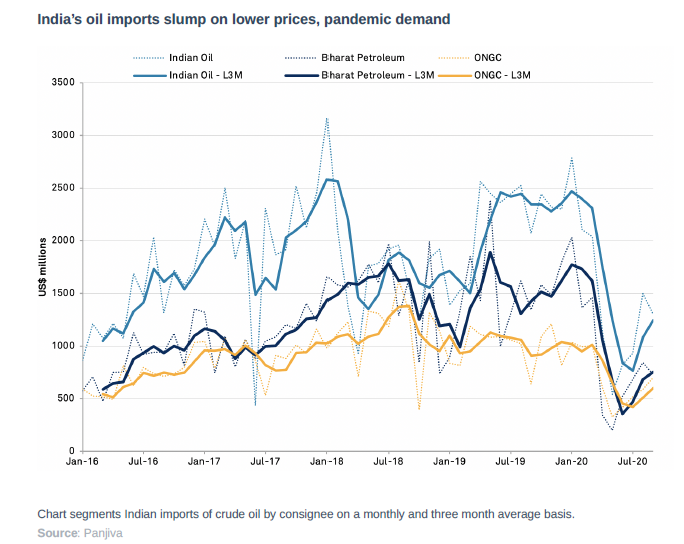

The event: While the COVID-19 epidemic spread to become a pandemic it wasn’t the only challenge facing global trade and logistics in March. A collapse in oil prices resulted from the drop in demand linked to the pandemic as well as a price war between Saudi Arabia and Russia.

Why it mattered: Oil accounted for 6.4% of global trade in 2018 while the oil price is a key component of the operating costs for shipping firms. The latter had also only just been through the process of switching to lower sulfur fuel sources.

What the data showed: For countries that are heavy net importers of oil the drop in price was something of a boon. Indian oil importers including Indian Oil, which accounted for 27.3% of Oil’s imports, and ONGC which represented 13.2%, have also been in the process of adapting their sourcing to bring more oil from the U.S. and less from Iran.

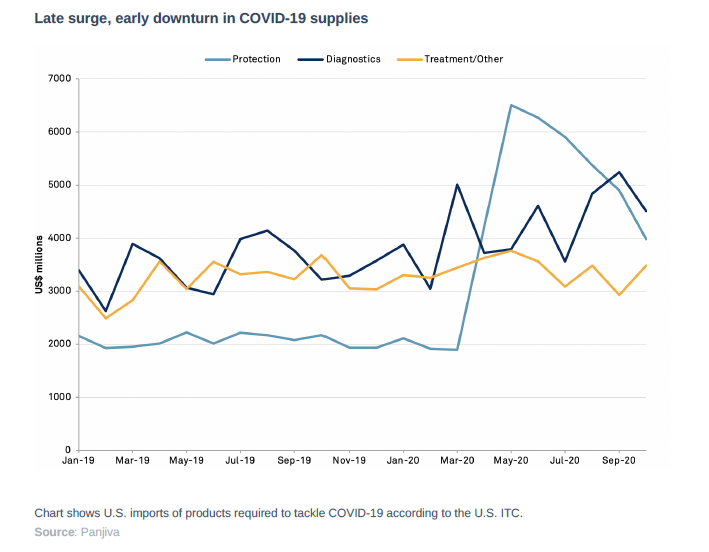

April – You don’t always get what you need – COVID-19’s impact on healthcare supply chains

The event: As the pandemic spread many governments engaged in medical protectionism with a view to ensuring sufficient supplies of PPE and ventilators, including by the EU despite a G20 initiative to ensure equal access to medical supplies.

Why it mattered: Aside from distorting global trade flows and allowing the rise of “medical diplomacy” by countries including China, the protectionism has led to moves by many governments to boost onshoring of production of critical supplies in the future. That may underpin policy decisions in the coming years, including state support that is even being considered in the U.S.

What the data showed: U.S. imports of PPE and ventilators fell during March compared to Q4’20 and only really got up to speed in July. Since then there has been a downturn from peak levels as national stockpiles, particularly of ventilators, have been restocked.

May – Food supply disruptions during COVID-19 – three issues to watch

The event: We naively assumed that the supply chain impact of the pandemic would begin to wane in June. One sign of continued disruptions could be seen in food supply chains with the temporary rise of food protectionism, including grains, while another was the disruption of packaging caused by the need to meet retail rather than food service demand. The U.S.-China trade war began to distort trade flows in meat. More latterly of course, Chinese concerns about the transmission of SARS-CoV-2 on packaging has been a further distortion.

Why it mattered: Food security is a huge issue at the best of times, but the regulatory risks caused by the U.S.-China trade war has raised questions about the operation of global protein supply chains.

What the data showed: U.S. exports of pork to China started to surge as soon as April as the phase 1 trade deal and ongoing shortages caused by the Swine Flu pandemic got underway. That growth has continued late into the year.

June – UPS beats the pack pack, Ceva continues to suffer as COVID-19 weighs on forwarders

The event: While the latter part of the year has seen a boom in logistics activity and congestion across the equipment, carrier and port space it is easy to forget that during the depths of the crisis there was widespread factory closures and consumer demand destruction.

Why it mattered: The logistics industry showed unprecedented discipline in managing available capacity in marine shipping while the closure of passenger air transport led to an involuntary reduction in belly hold capacity for airfreight. The latter has led to the advent of “freighters” later in the year.

What the data showed: Freight forwarders meanwhile had to deal with a drop in seaborne freight which reached a 19.7% year over year decline in May which acted as a drag on almost all players in the industry in their Q2 earnings.

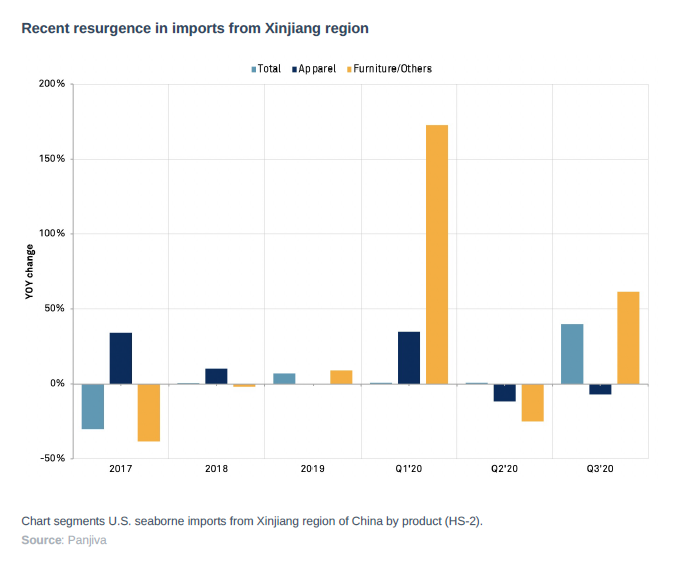

July – Lenovo, Alstom face supply chain choices after Xinjiang Entity List ruling

The event: While the phase 1 trade deal may have resolved tariff tensions, the U.S. continued to apply sanctions against Chinese actions in the Xinjiang region in relation to alleged labor abuses and in Hong Kong in relation to the new national security act.

Why it mattered: The bulk of sanctions have related to the apparel industry and paramilitary organizations in regards to Xinjiang, mitigating the impact on wider supply chains. Yet, late in the year there are indications that the actions may widen further. President-elect Biden is also set to continue a tough-on-China stance even though the tactics may change.

What the data showed: The U.S. government applied sanctions to 11 entities initially. Panjiva’s data shows that imports linked to the 11 entities fell by 66.9% year over year in Q2 and by 20.3% in 2019 versus 2018, including a reduction in shipments linked to Danby Products and Costco.

August – Cosco, CMA CGM face antitrust review as rates surge, China-LA volume hits record

The event: The Chinese Ministry of Transport started investigating surging container shipping rates after a 25% rise in China-U.S. west coast rates in just a dozen weeks.

Why it mattered: China’s move was just the first of many government attempts around the world to address soaring shipping rates as the recovery from an initial round of pandemic lockdowns got underway. More recently the U.S. Federal Maritime Commission is reviewing empty container booking practices, the South Korean government pressured liners to add capacity and India’s government launched a new bill to require increased rate transparency. The issue may continue to haunt the container-lines into 2021.

What the data showed: Container shipping rates outbound from China have increased by 60.7% year-to-date as of Dec. 18 according to Shanghai Shipping Exchange data. Transpacific rates rose by 80.0% from their trough while Asia-Europe rates have jumped by 78.4% from their low point in the spring.

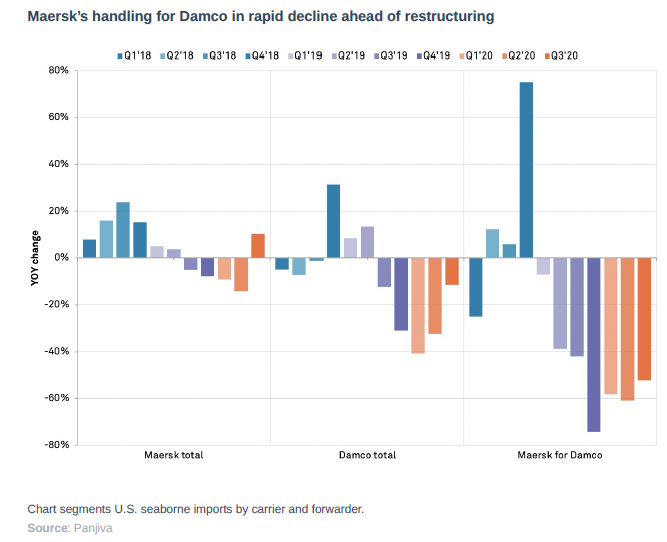

September – Maersk ditches Damco Damco, raising Ceva questions for CMA CGM

The event: A focus on dealing with COVID-19 has kept the widening consolidation seen in 2018 and 2019 in the shipping industry off the agenda. That didn’t prevent Maersk from restructuring its freight forwarding operations however, merging Damco’s seafreight operations with Maersk’s container line operations.

Why it mattered: Vertical integration and investment in new technology may prove to be a critical part of the logistics industry’s long-term recovery from the volatility caused by the pandemic and the U.S.-China trade war. Maersk’s action also caused DB-Schenker to boost its competitive pressure against its European competitor while also raising questions for CMA-CGM’s strategy for Ceva Logistics.

What the data showed: Damco has driven little extra business to Maersk with the container line representing just 13.9% of Damco’s operations on U.S.-seaborne import lines in the past 12 months to Aug. 31 compared to 32.8% in 2016. Ceva has been more successful recently with a 24.1% year over year expansion in U.S. inbound shipments in the three months to Aug. 31. CMA CGM also accounted for 23.6% of Ceva’s shipments in the past 12 months after a 93.0% surge in handling in the past three months.

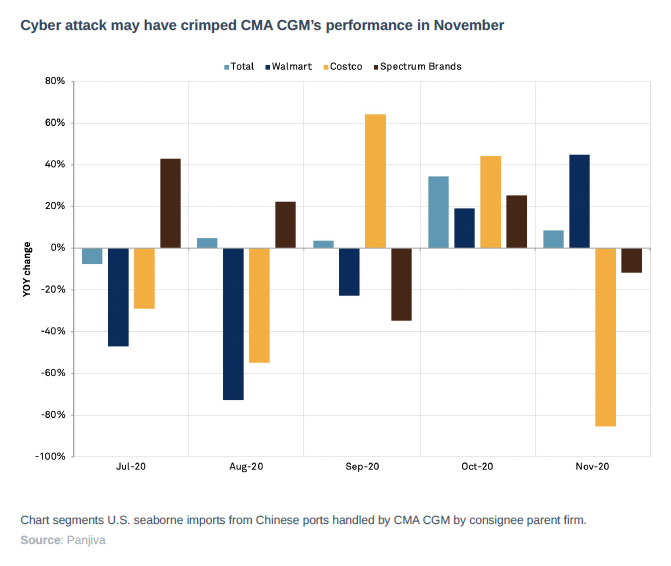

October – CMA CGM cyberattack comes during peak season for retailers

The event: As global trade activity began to surge in the fall, CMA CGM was hit by the “Ragnar Locker” ransomware attack that took down its operations around the world. It took nearly two weeks for the firm to fully recover its operations back to normal.

Why it mattered: The move to digital operations is a necessary part of the long-term development for the logistics industry, widening the risks from cyber-security breaches. CMA CGM joined Maersk, FedEx’s TNT, MSC, Toll Brothers and the IMO in suffering attacks in the past three years.

What the data showed: Major users of CMA CGM’s shipping services from China to the U.S. include Walmart, Costco and Spectrum Brands. Total U.S. seaborne imports handled by CMA CGM only increased by 8.5% year over year in November after a 34.4% surge in October.

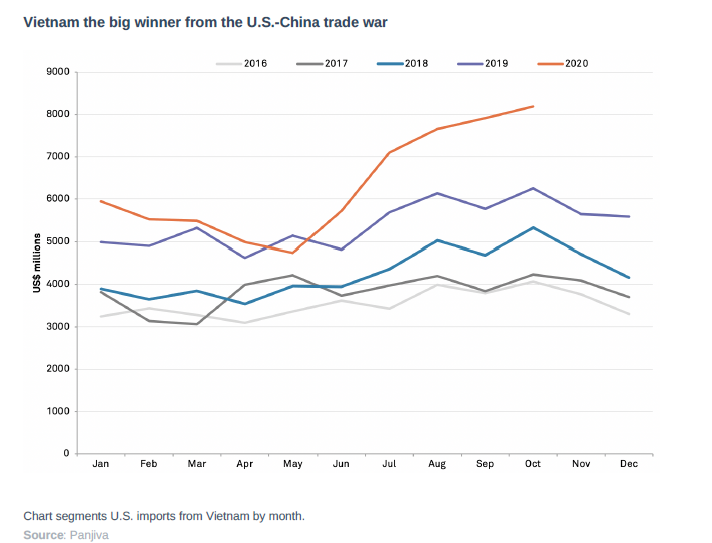

November – Life after the elections: 5 trade issues to watch to inauguration and beyond

The event: President-elect Biden won the U.S. general elections, raising questions about the future development of trade policy. The Biden administration will likely be characterized by: a continued tough-on- China stance; rebuilding of multilateral agencies; reduced trade frictions with allies including the EU; and the closer incorporation of labor and environmental standards into deals. Yet, Biden’s ability to deliver on policy will be limited by the complexion of the Senate, which awaits the outcome of the Georgia elections.

Why it mattered: The Trump administration has been marked by a shift in trade policy to bilateral, transactional deals, the aggressive use of tariffs and a turning away from multilateral institutions including the Paris climate deal, the WTO and trade deals such as TPP. Successes include a new approach to China and the negotiation of KORUS and USCMCA. A move to a more “boring” period of trade policy may reduce planning uncertainties for supply chain operators.

What the data showed: One of the biggest winners under the Trump administration has been Vietnam with U.S. imports having climbed 19.1% in the 12 months to Oct. 31 compared to the level seen in 2016. Near the end of the year the administration has sought to address that through a section 301, currency investigation which will leave diffcult questions for the Biden administration to address.

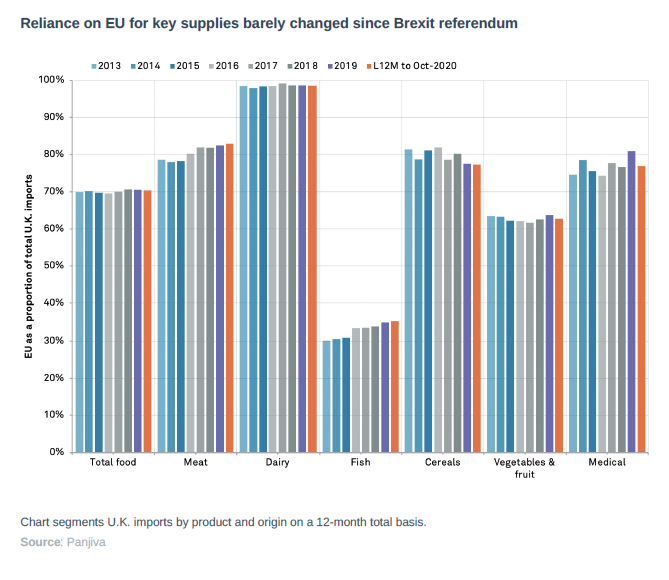

December – Brexit Watch: B.1.1.7 highlights risks to U.K. food, medical imports

The event: The U.K left the EU on December 31 with a new Trade and Cooperation Agreement after a saga that started with a referendum on mid-2016. The two sides spent the rest of the year attempting to formulate a new trade and customs deal with ongoing hang-ups centered on the level playing field of state support for industry, governance and fisheries.

Why it mattered: The first major example of a country leaving a free trade area will have repercussions for supply chains across Europe and beyond. While there will be zero tariffs there will be significant customs issues as new bureaucratic measures come into place while uncertainty on ratification of the bill and implementation of regulatory measures will complicate supply chain planning throughout 2021.

What the data showed: Near term disruptions to customs in Q1 were foreshadowed by port congestion in Q4 caused by the global shipping boom, stockpiling caused by deal negotiation uncertainties and a block of government medical supplies at Felixstowe. A simultaneous emergence of a new variant of COVID-19 closed border crossings, likely causing disruptions to the 70.3% of food and 76.9% of medical supply imports to the U.K. that are sourced from the EU.